Recently the Fair Money Advice team took a trip to Madrid to collaborate with the Nantik Lum foundation. The trip was primarily an opportunity for FMA to complete the training of the wider Nantik Lum team following their two -day visit and immersion to Fair Money Advice offices in London in February. It was also a good opportunity for the teams from both organisations to get to understand each others challenges and learn from each other, Fair Money Advice with 20 years’ experience of the debt sector in the UK and Nantik Lum with experience of working with entrepreneurs and the self-employed on financial education and who are now looking to work with those facing debt issues in Madrid.

On the first day of our trip we were welcomed to the Nantik Lum office in the fancy tech city, by their 9 strong team. The team introduced themselves and we got an insight into what they currently do which includes online courses, a career programme and financial advice for entrepreneurs and self-employed people. It appeared the clientele differed to those of Fair Money Advice back in the UK. Fair Money Advice’s clients are often those in crisis, they are financially struggling, and the service they require is not just financial education but often intervention and advocacy. Nantik Lum are growing and want to reach similar groups and assist them in Spain and this is where Fair Money Advice stepped in, to share with them our experience in the debt and financial resilience services sector over the last 20 years and what they can possibly learn from it.

Our services manager Jahanara started by giving them an overview of what we do and explained that we are similar to them as we also look to educate our clients through the service we offer. Jahanara explained how we rely on partnerships to deliver debt advice and these include local authorities and housing associations, amongst others. One way we have been successful in achieving these partnerships is by presenting to the other party how our service can actually benefit them. For example demonstrating to stakeholders that preventative measures with a client can actually save them money in the long term – a cost –benefit analysis approach. Doing a ‘financial health check’ with a new social tenant and ensuring they are receiving the benefits they’re entitled to, they are aware of how much rent they need to pay, what frequency and ensuring they budget for this can help avoid them falling into arrears early on in their tenancy and set up good practice for the future. The financial health check was a successful programme we had with partner housing associations and we explained to Nantik Lum that if they can access the relevant data, highlight structural barriers and bad practices they can also make their case to stakeholders for assisting their clients.

The Nantik Lum team fed back to us that such partnerships with social landlords and local authorities in the Spanish context would be very difficult. This was a reminder that at one point in the UK there was also the same issue however the debt advice sector is much more mature in the UK, it is regulated and recognised. In Spain there is currently no structure for debt advice and this will present the Nantik Lum team with challenges. Fair Money Advice had also gone through these challenges when the UK debt advice sector wasn’t what it is today and our experience of how we overcame these challenges will hopefully better prepare the Nantik Lum team.

Jahanara spoke more on the services we offer along with the financial health check such as debt advice. She explained how in both services we require a lot of information from the client however the debt advice side is a lot more invasive. The Nantik Lum staff raised this as another issue they have, getting their clients to provide all the information required. They said the clients will often not provide physical proof and they have to rely on what the client tells them and trust this. They understand that clients are actually scared to share this information, for example they’re worried that informal income could affect their access to social benefits. They wondered if there was a cultural aspect.

From our perspective we advised that the issue of getting information and proof from clients will get better with time and experience. Advisers need skills so they can build the confidence and trust of the clients in them, these are often gained through experience and dealing with clients. Once an adviser actually has more confidence themselves in their role, they will be in a better position to explain to the client why they need the information so they can help them. This takes us back to the point about explaining to stakeholders how we can actually help them so they let us assist their clients, it’s the same principle.

An important point made by our managing director Muna on the issue of building trust with the client, is that the staff should reflect the community they’re serving. If advisers are familiar to clients it can not only help gain clients trust but it can also be very practical as the adviser may share a language with the client and this could be one of the barriers the client faces when it comes to accessing services. This leads on to another point we shared with Nantik Lum that one of our strengths is that we are a smaller organisation. Initially you may not think that being small would be a strength but when you consider that Fair Money Advice provides services in London only it means that the advisers can really know the context they’re dealing with. Being ‘small,’ ‘local’ and a ‘community organisation’ bring great benefits as they bring essential knowledge such as knowing where to refer a client if you recognise another issue they have or understanding local specific issues that affect the clients. Nantik Lum are similar to Fair Money Advice in this way as they are Madrid based and serve clients in the city.

Next our debt adviser Soomaiya went through one of our essential tools with the Nantik Lum group, the Financial Statement. The financial statement records all the client’s income and expenditure details. Soomaiya explained that where an adviser can they will need to request proof of income and expenditure as this ensures the adviser is presenting a realistic idea of the client’s financial situation to the client and creditors if need be. In the UK it is also important that an adviser has this information on file as the UK debt advice sector is regulated, files can be reviewed and the adviser may be asked where they got the information they entered in the statement.

The financial statement and clients providing documents for this brought us back to the issue of clients unwillingness to provide this information in Spain. Another issue the Nantik Lum staff raised with the creation of a financial statement based on the information the client provides is that often they have found clients are not actually aware of where they are spending and they lose track. When the client’s information is unreliable it is a worry that the financial statement may not reflect reality. In this case again we explained the benfits of letting the client know how they can be helped if they cooperate and provide the information. If you have a copy of the client’s bank statements it is easier to see where they are spending and if they are overdrawn or in credit at the end of the month. We also discussed with them how the financial statement can be used as an aid for better financial behaviour going forward. It can be used as a budgeting tool by presenting to the client what their income is and how much they can afford to spend on different areas.

Our first day came to a close and it was obvious that there was still so much the Nantik Lum team wanted to ask. Luckily we had an evening meal planned with them where we could discuss things further in a more social setting plus we got to enjoy some delicious Spanish cuisine!

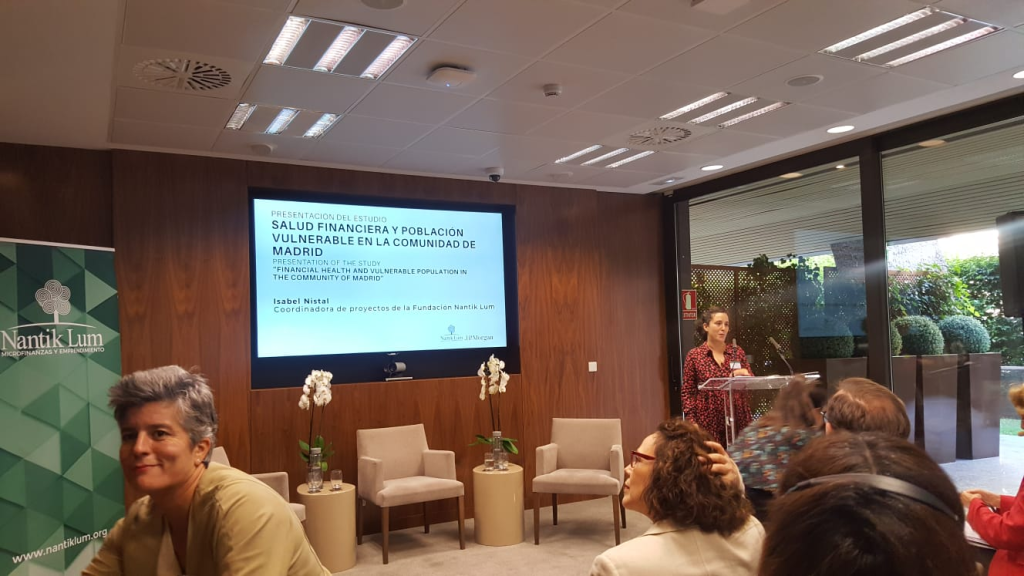

Our second day in Madrid was the big day, the conference! The conference was hosted by JPMorgan Madrid and a chance for Isabel from Nantik Lum to launch their study ‘Prevention of over Indebtedness of Vulnerable: Improve Financial Health’ and findings to potential funders and partners. Our very own Muna was also presenting to give the Madrid audience an insight into the journey of Fair Money Advice and an overview of the UK landscape and context. Alongside Fair Money Advice and Nantik Lum there were presenters from academic, banking and other third sector organisations as well as a representative from the regulator in Spain – the Central Bank The conference was also an opportunity for us to learn more about Madrid, the issues and need for a service such as debt advice.

We learnt that the average rate of financial literacy across Europe is 52%, in Spain 49% of the population is financially literate and in the UK it is 67%. Although Madrid is the driver of economics in Spain, 17% of it’s population is considered poor. This is around 1.1 million people some of which are trying to survive on 500 euros a month, which is very challenging. With the growth of wealth there has also been a growth in poverty and there are approx. 3,000 homeless people in Madrid.

Financial Education was discussed as a way of tackling the issues of the financially vulnerable. There was an emphasis on making solutions holistic and designing ‘products’ for the target audience to meet their needs and make them easily accessible. Muna highlighted the importance of client segmentation to help tailor services to clients. The Money and Pensions Service (MAPs) in the UK have segmented UK consumers into three key groups. This has greatly aided the design and delivery of financial education and resilience services in the UK as they can be designed with a particular group in mind. Muna noted that the advantage of segmentation -on a national scale - meant data wasn’t just in the hands of the commercial sector like banks and large creditors who do this internally for their customers. When talking about tailoring things for specific clients issues of ATM access and bank branch closures were also mentioned and the trend of moving to digital in the financial sector potentially creates a new group of financially excluded individuals, those who are not ‘tech savvy’ in particular the older generation. Branch closures and the move to digital are also reflected in the UK context and it has presented issues for Fair Money Advice’s clients. At the end of her presentation one of the questions Muna was asked was if technology was a friend or foe to which she replied that it was a friend but for vulnerable clients groups it can’t be used on its own without sufficient support packages . The necessary support needs to go alongside the technology to ensure inclusion and financial capability.

Nantik Lum’s Isabel presented how their project had looked at training social workers to work with the financially vulnerable population to give them the tools they need. Some of the tasks the social workers carried out with clients were looking at reducing their costs, so reviewing their bills and seeing where they can save and making an economic plan with a budget.

Isabel also gave more of an insight to some of the financial issues of Madrid’s citizens and why a service like theirs is needed. 6% of homes in Madrid have been late in paying either their mortgage, rent or bills and 30% spend more than they receive.

One of the findings of working with this group of people was that they recognise their debt is a problem when it is too high and they can’t act. We would describe this as a crisis point and we see the same issue with clients in the UK. They found that to deal with these issues clients had taken out illegal loans to pay for basic costs. Again this is another issue we can relate to and was particularly a problem when there was little regulation around ‘pay day loans.’ As Muna put it later on in the event ‘regulation in the UK has driven many bad lenders out of the market.’ So along with the work of organisations such as Nantik Lum on the ground, the regulator also plays a role in improving the wellbeing of the financially vulnerable.

Isabel also mentioned how the social workers don’t make recommendations when it comes to saving. As mentioned earlier by another speaker the idea to save 20% of your income is important but some Madrid residents are struggling to survive on 500 euros a month so saving for this group is not the solution. Instead of focusing on savings, the social workers will look at how the client can manage what they do have and this brings us back to the point of tailoring services to the client’s needs and capabilities.

Based on the information Isabel presented it is clear there is a need for the training of social workers to assist the financially vulnerable in Madrid. The need for training the social workers was also recognised as through the project Nantik Lum found that the social workers before training had been unable to identify those at risk, didn’t know where to refer them to or know how to obtain something called a ‘social voucher’ which can assist those struggling to pay their bills.

The trip to Madrid was thoroughly enjoyable for the Fair Money Advice Team and not just because of the sun and the break from the awful British weather! On reflection we all said a highlight had been meeting the Nantik Lum team, how warmly they had greeted us and how it was nice to be in a slower paced environment for a change! So although we went to Madrid to share our experience and hopefully for Nantik Lum to learn from us we can also take away from it some learning in hospitality and not always having to go at 100 miles an hour!